Andrew Walker recently had Matt Turk on his podcast where they discussed this idea. I generally agree, but for my own process, I wanted to write out my thoughts as well.

Target Hospitality (TH) ($1.2B market cap) is a provider of mobile temporary housing (previously colloquially called “man camps”) that historically focused on the energy exploration sector (about 1/4 of their business today) but over the last decade, and mostly in the last few years, TH has moved into the business of housing migrants crossing the U.S. southern border. Their largest contract is an influx care facility (“ICF”) called Pecos Children’s Center in Texas that houses unaccompanied minors, by law unaccompanied minors cannot be deported immediately and efforts need to be made to reunite them with family members. During this time period, which can last several years, the minors need reasonable and safe housing quarters. There is political risk in this business, for a while there these types of camps were called “kids in cages” and other politically charged terms. But with a large number of migrants coming from destabilized places like Venezuela, Ecuador and Haiti, the need for safe temporary housing doesn’t appear to be going away anytime soon.

The oil & gas housing business is not particularly great, Civeo (CVEO) is a good comparable, many oil & gas projects require significantly more employees (temporary residents) during the beginning of projects and relatively few are needed during the maintenance periods, putting the business at the whims of commodity cycles. But with government contracts, contracts tend to be longer in duration, my mental model for the unaccompanied minors camps is more inline with government contractors that provide services to foreign U.S. military bases in conflict zones. Something like V2X (VVX, fka Vectrus, a spin from XLS) comes to mind, there’s a continuous need for occupancy as long as the need is there and that need typically lasts longer than the public expects at the outset.

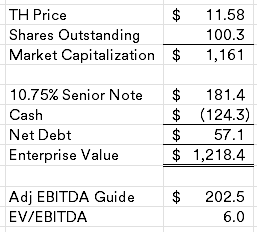

Target Hospitality is currently fairly cheap at only 6x EBITDA with minimal debt (management projects to be in a net cash position by year end).

CVEO and VVX obviously aren’t perfect comps, but I’ve owned both businesses in the distant past and follow them loosely, CVEO trades for 5x EBTDA and VVX trades for 8.5x EBITDA. Blending the two based on Target Hospitality’s business mix gets me something closer to a 7.5x multiple or a $14.50 share price.

TH is a former 2019 vintage SPAC (before all the craziness) and is still 65% owned by Arrow Holdings (now TDR Capital), TDR Capital submitted a bid on 3/25/24 to buyout the minority shareholders for $10.80/share. The following day, Conversant Capital (same firm that was involved with Indus Realty (INDT) and currently the controlling shareholder of Sonida Senior Living (SNDA)) popped up with a 5% ownership filing with the below disclosure:

As previously disclosed in its filings on Form 13F, Conversant Capital LLC has owned a substantial position in the Company Common Stock for approximately two years, in the form of shares of Common Stock and options to purchase shares of Common Stock. As long-term investors in the Company, the Reporting Persons closely monitor developments regarding the shares of Common Stock. The reporting persons are aware that TDR Capital LLP (“TDR”) has made an unsolicited non-binding proposal to the Board of Directors of the Company pursuant to which Arrow proposes to take the Company private by acquiring all of the outstanding shares of Common Stock, other than those already owned by any of Arrow, any investment fund managed by TDR or their respective affiliates. The Reporting Persons intend to review that proposal and any other proposals made in connection with their evaluation of their investment in the Company to evaluate whether any such proposal is in the Reporting Persons’ best interests.

In TDR’s offer letter, they’re requiring their offer receive a majority of the minority shareholders vote for the deal, with Conversant a large and now public shareholder, they provide credible protection against a take under. A special committee was formed on 4/29/24 to consider the offer, the press release also mentioned the following:

The mandate of the Special Committee is to consider and evaluate the Proposal and any alternative proposals or other strategic alternatives that may be available to the Company. The Special Committee has retained Centerview Partners LLC and Ardea Partners LP as its financial advisors and Cravath, Swaine & Moore LLP as its legal advisor.

Sounds like a full process could be underway and not just an exclusive negotiation with TDR Capital. If nothing comes of the process, I still think the shares are cheap as the company has vaguely discussed being in the procurement stage on several large contracts including another ICF/unaccompanied minor location, rare earth mines, large technology projects, etc. Several of which have been described as “impactful” on earnings calls. In total, they expect to generate $500MM in free cash over the next several years that will be used to deploy into new growth opportunities which could further diversify the business model, potentially further raising the multiple.

Disclosure: I own shares of TH