Back from the Easter break with 20 freshly selected random Belgian stocks. This time, four made it onto the preliminary watch list.

81. MAATSCHAPPIJ VAN DE BRUGSE ZEEHAVEN (Expert Market)

At first I got excited, as this seems to be the Port of Brugge and the port seems to have grown over the years according to Wikipedia. And I do like ports.. But this stock traded last in 2015. It seems that at a higher level, the port has already merged with Antwerpes.

Unfortunately I did not find any financial information. “Pass”.

82. Mazaro NV

This 4 mn EUR market cap company seems to be (or have been) an automobile supplier. They IPOed in 2022, but seem to have not reported any figures in 2023. This looks strange, “pass”.

83. CFE

CFE is a 190 mn EUR market cap company engineering and construction company, majority owned by Belgian HoldCo Ackermans & Van Haaren (62%). French construction company Vinci owns an additional 12%.

I came across CFE earlier as CFE was a partial owner of DEME (which I own) but they spinned of the stake in the IPO to their shareholders

The margins have decreased over the years, but the stock is very very cheap.

Interestingly, they were relatively optimistic for 2024 in their outlook in the results presentation. I will “watch” them as part of the AvH family.

84. CP76 & CP79 Petrofina (Expert Market)

There is also a CP 79 PEtrofina on the Expert market. Both traded last in 2020. They seem to be some kind of remainder from former Belgian Oil company Petrofina, but I didn’t find out more. “Pass”.

85. Hyloris Pharmaceutical

Hyloris is a 310 mn EUR market cap pharmaceutical company that has very little sales (3 mn) but significant losses. They seem to be public since 2020 and the stock price now is roughly at the IPO level.

I cannot judge at all how promising their pipeline is, therefore I’ll “pass”.

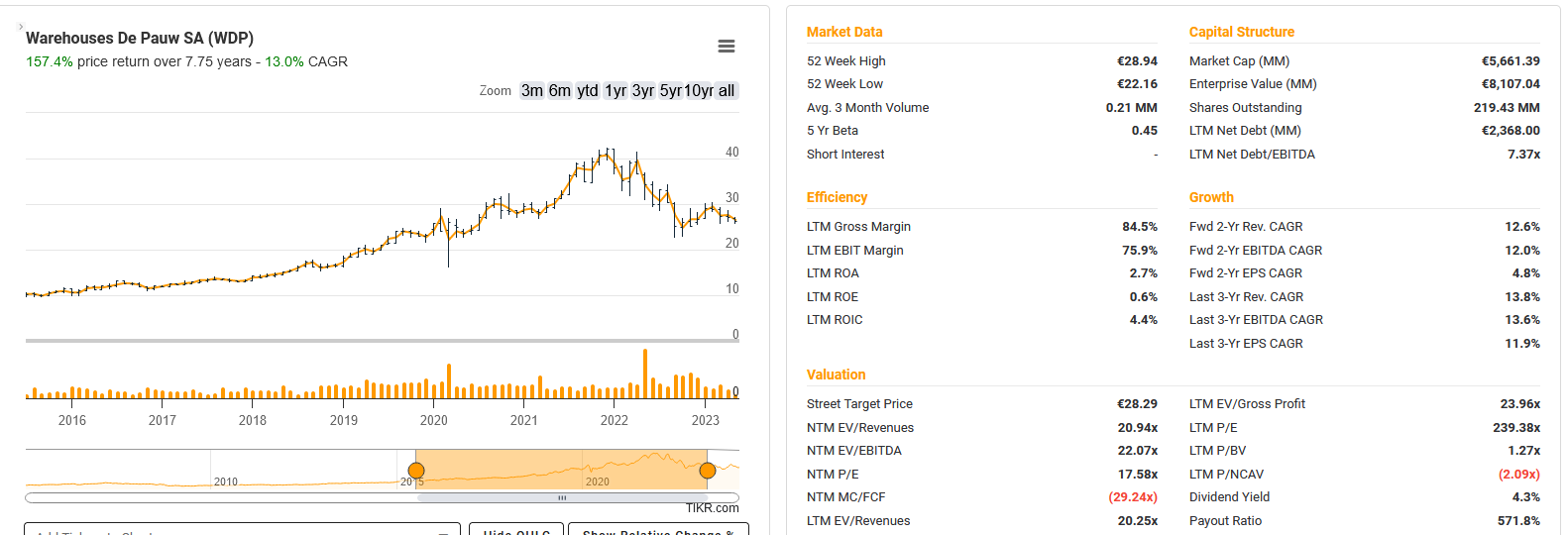

86. WDP (Warehouses de Pauw)

With a market cap of 5,6 bn, WDP is a larger player in the logistics real estate space. As this sector still performs quite well. The De Pauw family is still the largest shareholder with a stake of 21%. WDP is also significantly more expensive than for instance office focused real estate companies, despite a pull back in the share price:

However, also this sector is not of interest for me, so I’ll happily “pass”.

87. Ucare Services

This 0,25 mn EUR Pico-Cap seems to be a home care service that doesn’t release financial numbers any more. “Pass”.

88. MICS Partners (Expert Market)

The Euronext Expert Market page doesn’t record any trade for this one. “Pass”.

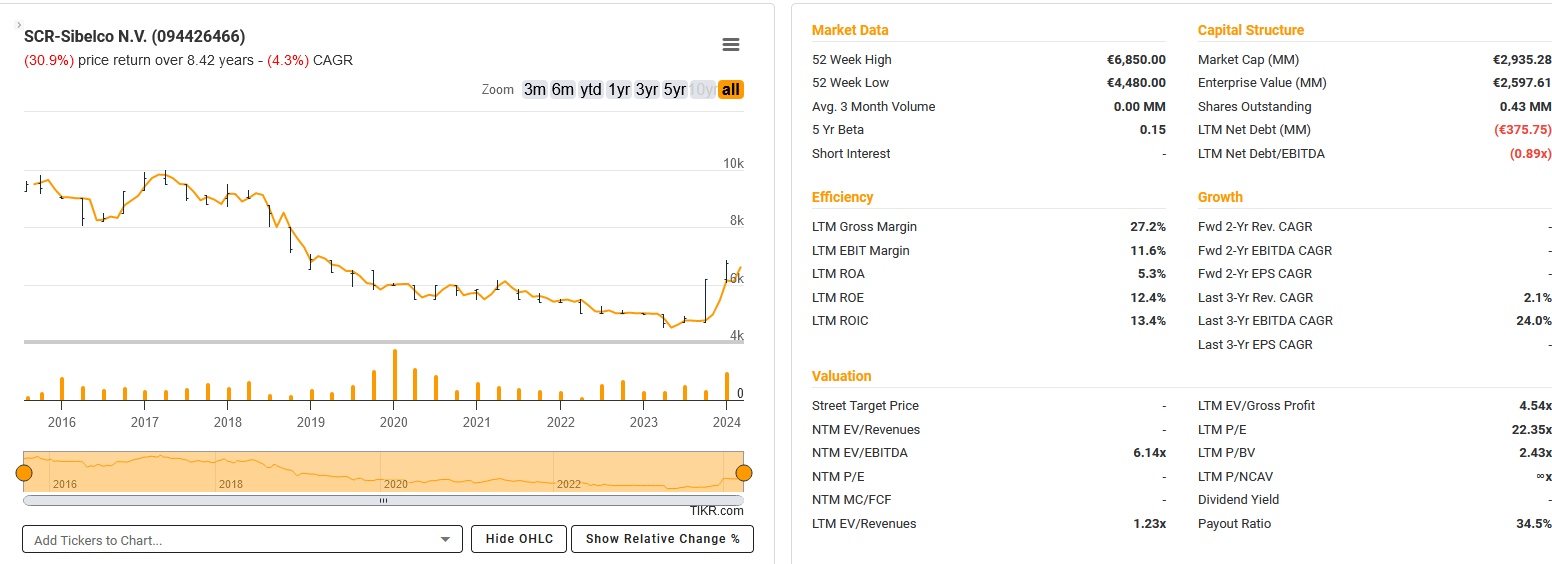

89. SCR-SIBELCO (Expert MArket)

SCR-SIBELCO is an Expert Market stock that trades quite regularly. According to TIKR, the have a market cap of 2,9 bn EUR which is a lot for an OTC stock:

The company is a minerals extraction/mining company, producing a wide variety of materials used among others by PV, Insulation etc.

Looking at that chart from their 2023 report, one can see that the business is quite volatile but 2023 has been a decent year:

They also seemed to have bought back a significant amount of shares in 2024. It would be really interesting to know why such a large company is not listed on the main exchange. But anyway, Mining is also not something that I know a lot of, therefore I’ll “pass”.

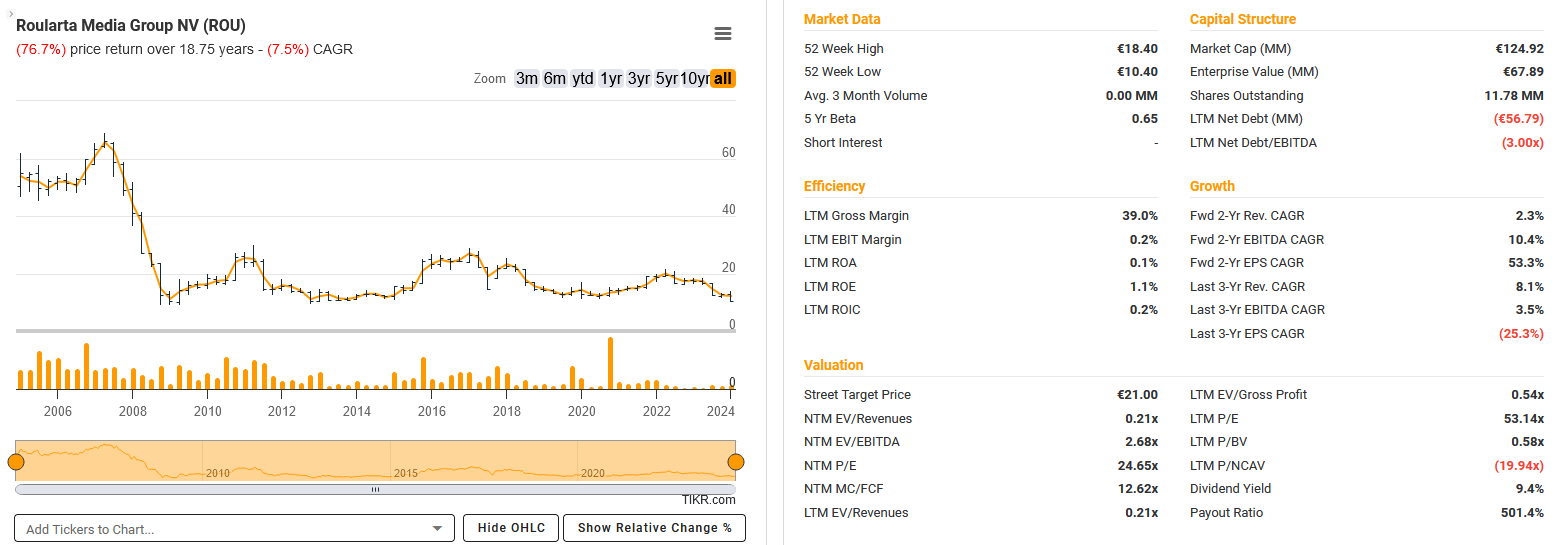

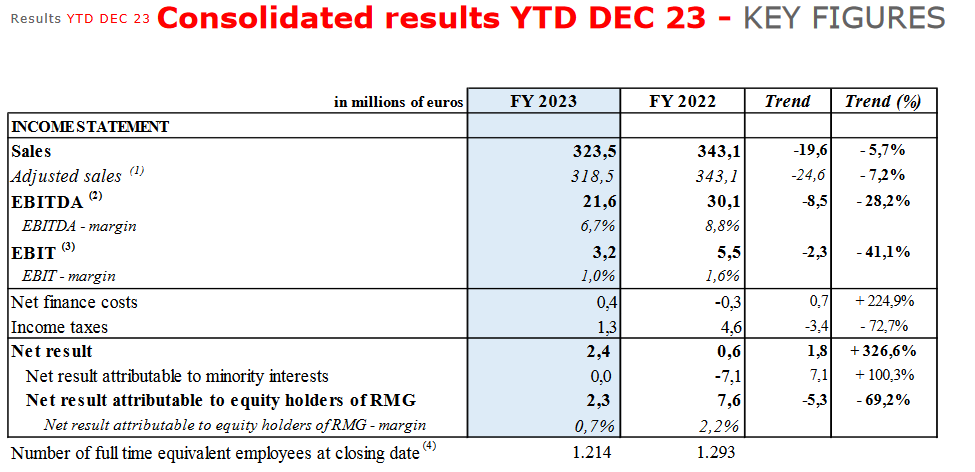

90. Roularta Media Group

This is a 125 mn EUR market cap Media company that (unfortunately) focuses on print magazines and seems to have seen better days:

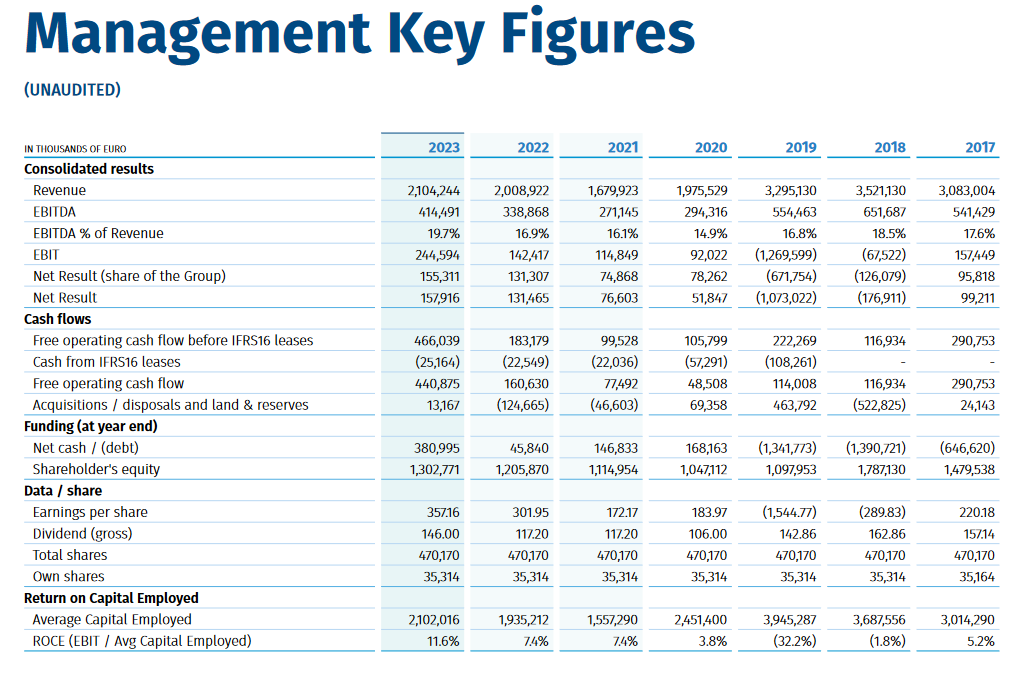

The 2023 results give a pretty depressing picture:

The company sits on some 60 mn of net cash, but that seems to deplete quite quickly, also via large dividend payments. Looks too much like a melting ice cube, therefore I’ll “pass”.

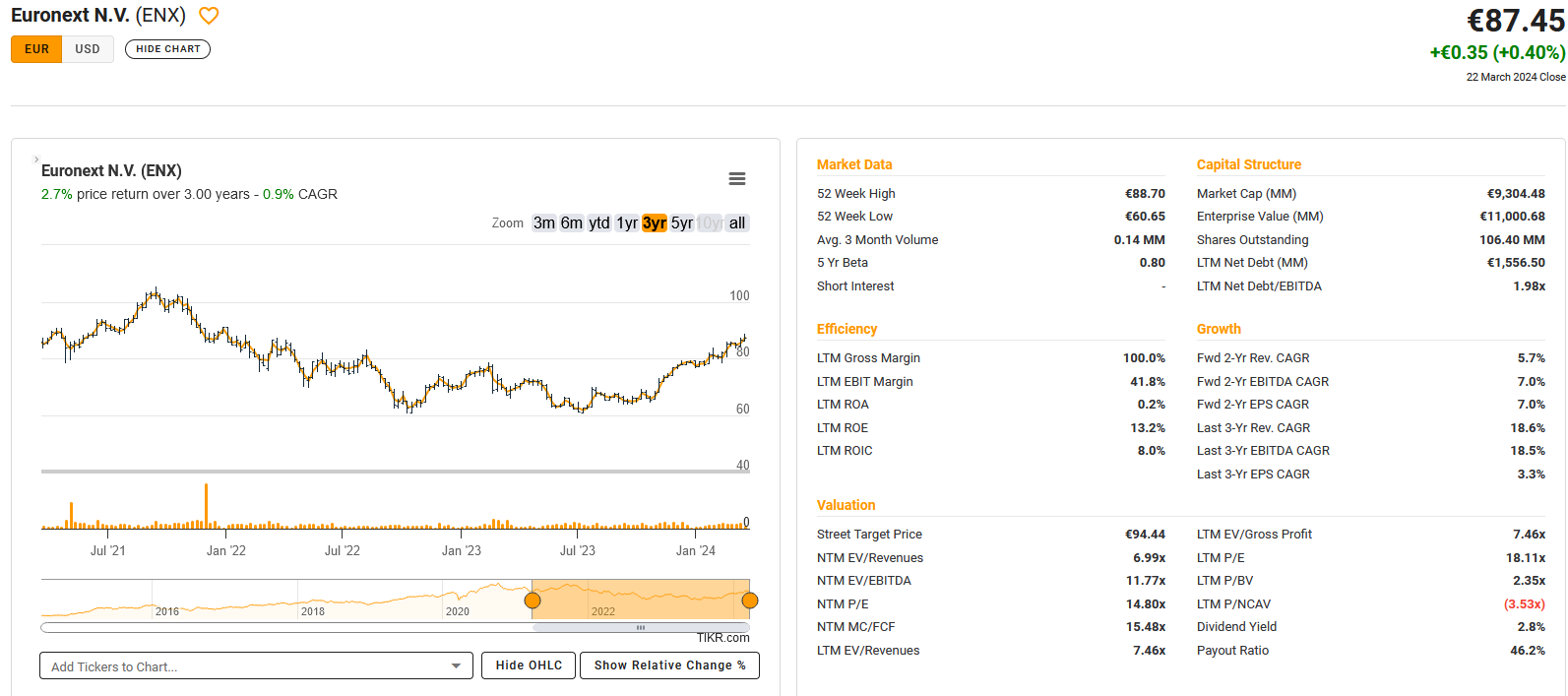

91. Euronext NV

Euronext, with a market cap of 9,3 bn EUR is another company that reader of my blog might know. I bought a small position in 2021 but excited it in early 2022 with a small profit as I could not build up enough conviction for a larger position.

The stock has been week for some time but has recovered lately to the level where I sold it in January 2022:

The business of running an exchange is normally a very good one, with the caveat that Europe overall has been somehow suffering from many take overs, delistings and few IPOs in the recent years.

Euronext enjoys very nice margins, 2023 was all in all OK, helped by a good Q4. For an exchange operator, the stock is not too expensive, although I don’t like all the adjustments they are making in presenting their numbers.

Nevertheless, this is clearly one stock to “watch”, especially if investor interest comes back to Europe.

92. BioCartis

BioCartis is a 27 mn EUR market cap Biotech company that has seen better days. the company is loss making and has significant debt. “Pass”.

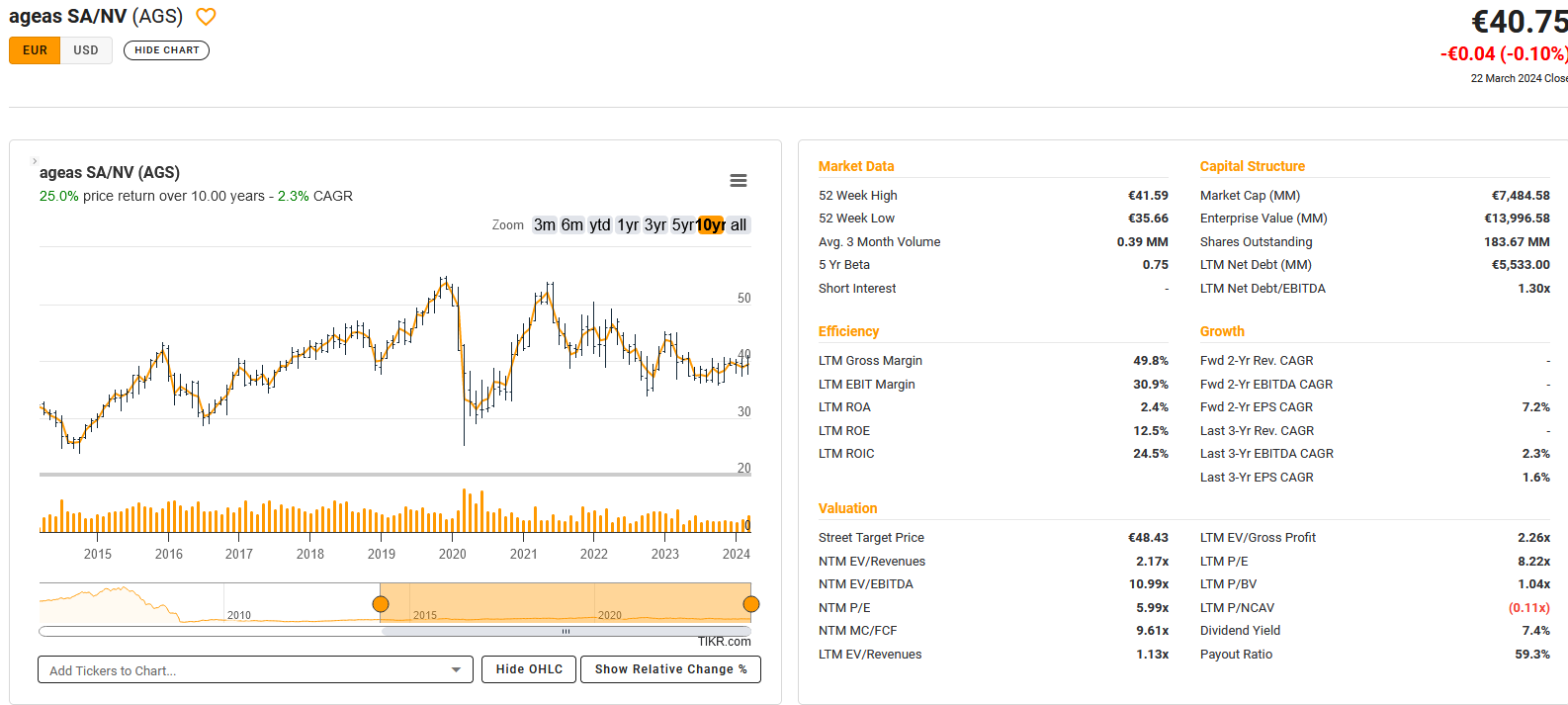

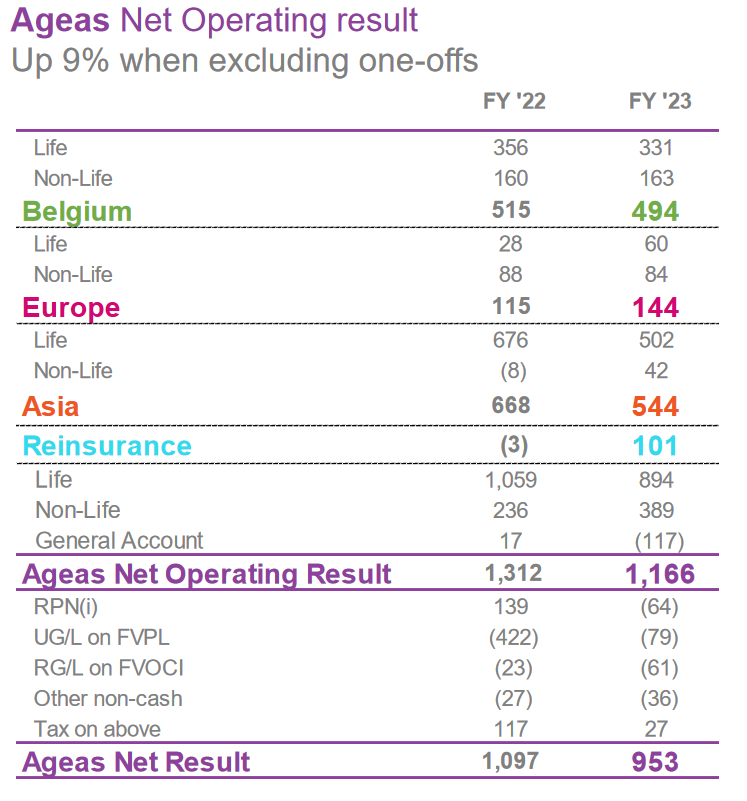

93. Ageas

Ageas, a 7,5 bn market cap stock, is the insurance arm of former Belgian Financial Conglomerate Fortis, which went down during the GFC.

Looking at the share price, we can see that nothing big happened over the past 1 years, however, they pay a very juicy dividend:

The company has been buying back shares (share count -10% over 6 years). Very recently, they made a move to acquire Direct Line in the UK but walked away as Management of Direct Line opposed the transaction.

Ageas is active in both, Life and Non-Life business. One very specific aspect is that around 50% of the operational profit comes from their Chinese Life Insurance business.

I think this also explains the low valuation, as investors clearly discount the earnings from China higher. The largest shareholder interestingly is the Chinese Fosun Group with ~7%. Ageas itself was always rumored to be a take-over target itself.

I will put them on “watch” although I also think that the high share of Chinese profits could be an issue.

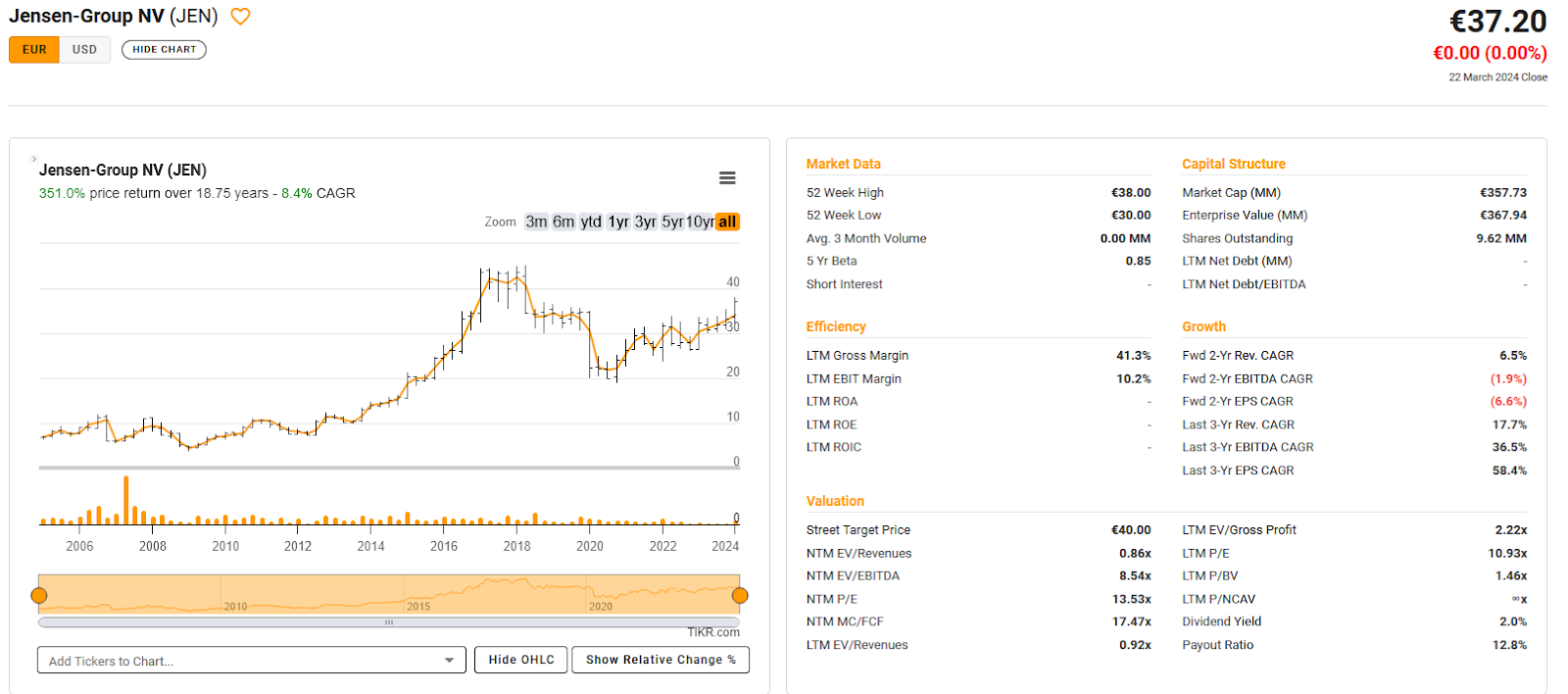

94. Jensen Group

Jensen Group, a 360 mn EUR market cap company is a specialist for “Heavy duty laundry” machines, so clearly not your typical household washing machine.

With the exception of Covid, jensen looks like a nice “slow grower”:

The stock is not too expensive and according to TIKR, the family still owns north of 40%. Interestingly, as the name indicates, the Jensen family is Danish.

2023 was a really good year for them. They also “swapped” a 20% capital increase with Assets from Miura, a listed Japanese company, in order to enter the Japanese market.

I had looked at the company before but I have to admit that now I find them really interesting. They will go on “watch” with some priority.

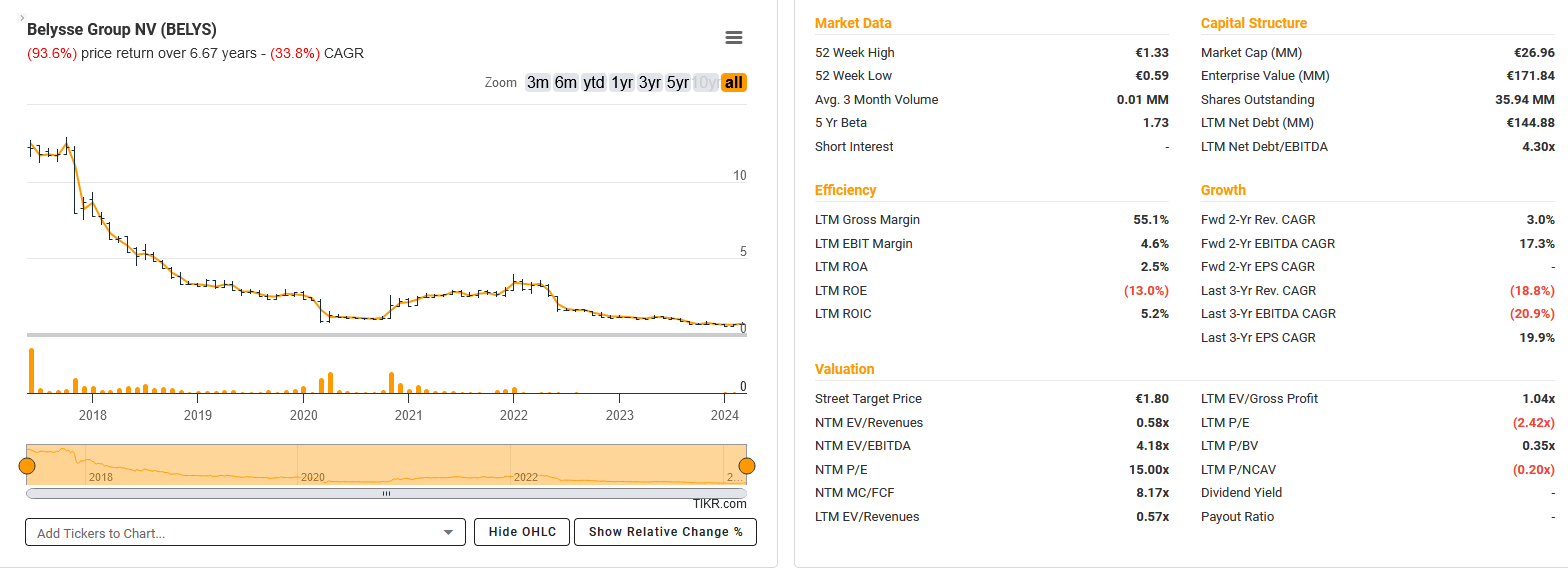

95. Belysse Group

Belysse (formerly Balta Group) is a 27 mn EUR market cap company that manufactures textile floor covering.

As the stock chart shows, they clearly had better times.

Sales have halved in Covid and never really recovered, the company made losses every year since then. %4% of the company are owned by Lone Star fund, a well known ”Vulture”. “Pass”.

96. Peltzer (Expert Market)

This Expert MArket stock seems to have never traded. “Pass”.

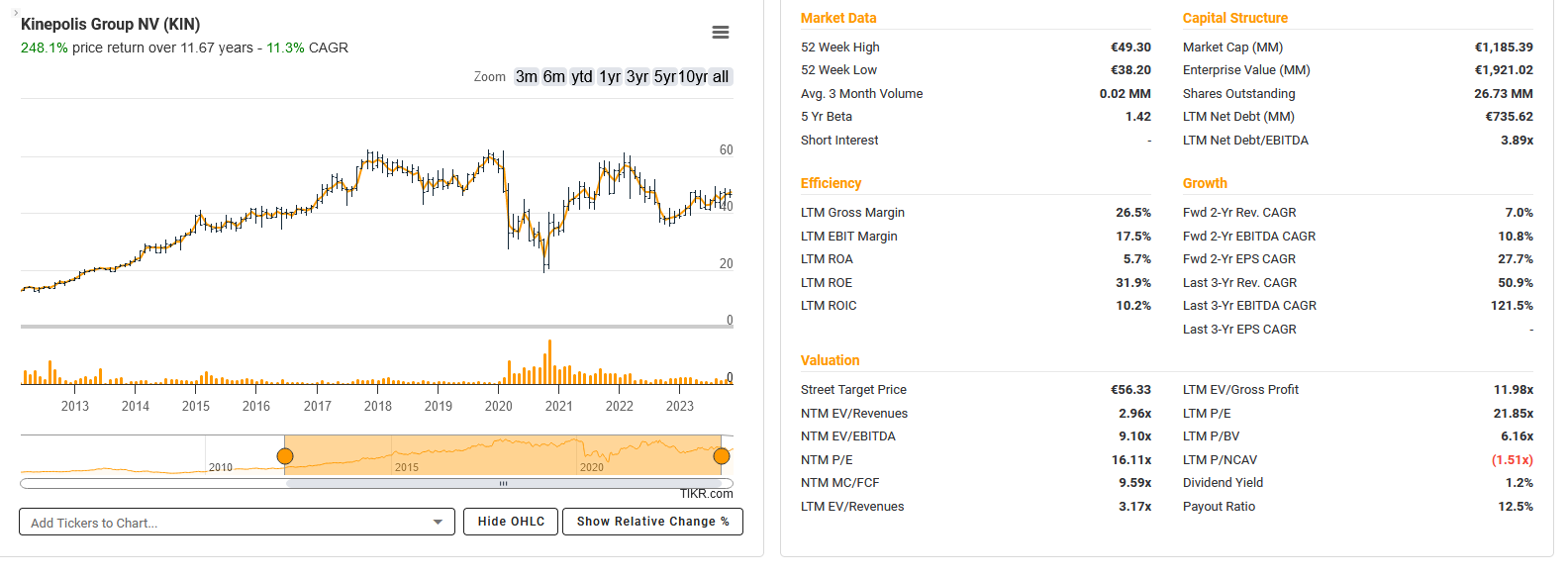

97. Kinepolis

Kinepolis is a 1,2 bn market cap operator and owner of movie theaters. Looking at the share price, they held up quite well since Covid despite the strong headwinds:

They are active in Europe and the US and run the IMAX movie theaters. The reporting is quite nice, but I am not 100% sure how much future the movie business really has, especially as the stock is not really cheap either. Maybe they could try their luck as meme stock, as their US peer AMC. “Pass”.

98. Surongo (Expert Market)

This stock traded last in 2018. Googling the name only reveals a Bollywood movie with the same title. “Pass”.

99. ABO Group

The Belgian ABO Group has nothing to do with the German ABO Wind (which I own). It is instead a 60 mn market cap Engineering Group that is active in “geotechnics, soil remediation, energy, and water and waste management solutions in Belgium, the Netherlands, France, and internationally.”.

To a certain extent it is a small competitor of DEME which offers similar services. They managed to double sales since 2016, but margins are thin and the valuation quite high with a P/E of 22x. Free float is small as 86% are held by one person. “Pass”.

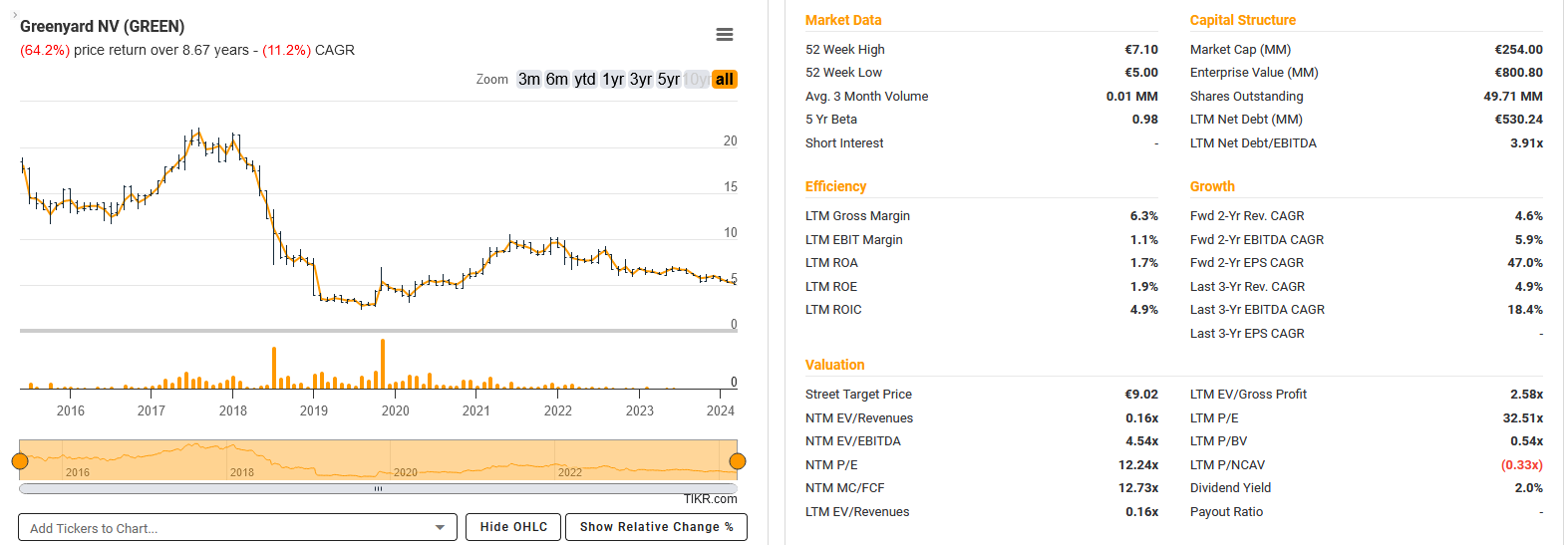

100. Greenyard

Greenyard is a 254 mn EUR market cap distributor of fruit and vegetables that also has seen better days:

The company carries significant debt. Margins are thin and return on capital is low. The investor presentation is full of adjustments. Positive: The CEO owns 44% of the company.

Overall, it doesn’t look very appealing and the high debt is an issue these days, “pass”.